Global Railway Sleepers Market Soars Towards USD 112.8 Billion by 2030; Driven by Urban Rail Expansions and Sustainable Material Innovation

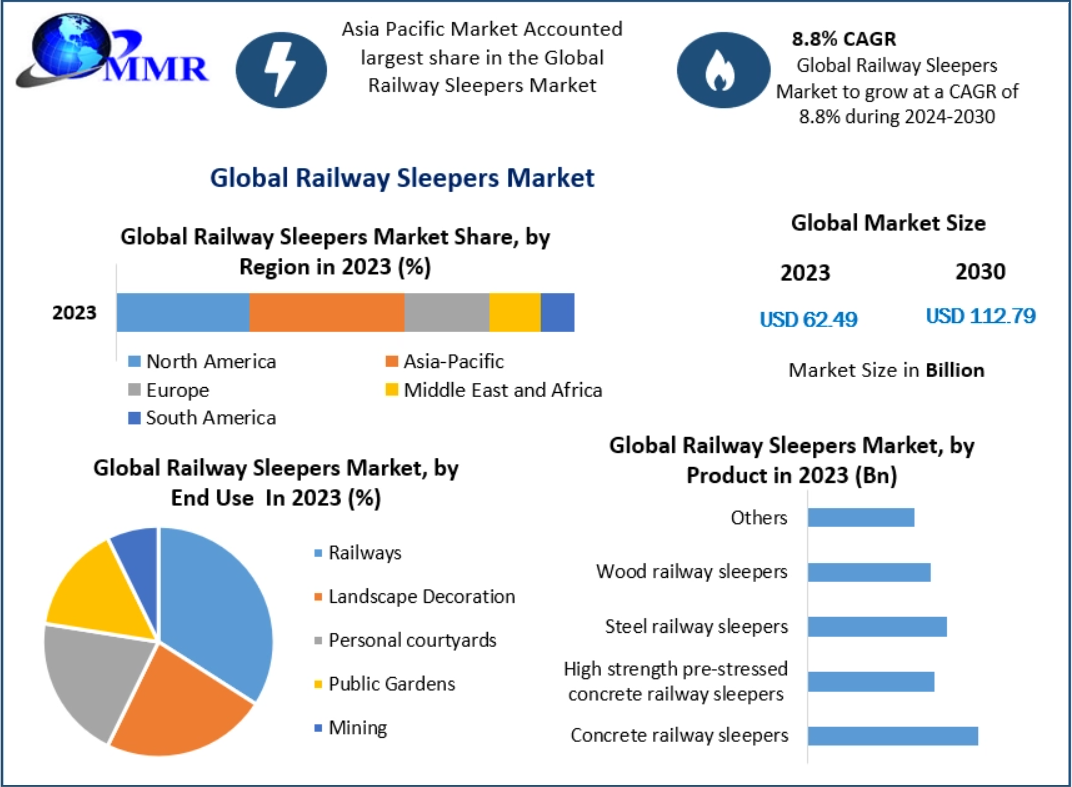

The Global Railway Sleepers (also known as railroad ties) Market is on a compelling growth trajectory, expected to surge from approximately USD 62.5 billion in 2023 to an estimated USD 112.8 billion by 2030, reflecting a robust compound annual growth rate (CAGR) of 8.8%.

Market Estimation & Definition

Definition:

Railway sleepers are the rectangular components laid perpendicular beneath rails to maintain correct gauge, distribute load, support structural integrity, and ensure safe, durable rail installations.

Market Estimation:

- 2023 base size: USD 62.49 billion

- Projected 2030 size: USD 112.79 billion

- Forecast CAGR (2024–2030): 8.8%

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/113617/

Market Growth Drivers & Opportunities

Key Growth Drivers:

- Rapid expansion of metro and subway networks in both emerging and developed economies is fueling substantial demand.

- Increased passenger rail traffic in developing nations is prompting infrastructure upgrades and modernization of aging networks.

- Cross-sector applications: Beyond traditional railway networks, sleepers are being used in landscaping, private courtyards, public gardens, and mining operations.

- Dominance of concrete sleepers due to their cost-effectiveness, durability, and lower maintenance requirements compared to traditional wood or steel.

Growth Opportunities:

- Technological innovations such as photovoltaic-integrated sleepers present new opportunities, allowing railways to integrate renewable energy into infrastructure.

- Sustainable and recycled materials such as composite and plastic sleepers are increasingly being adopted to align with green construction practices.

- Expansion of light rail transit (LRT) systems creates demand for specialized sleeper designs tailored to urban mobility needs.

- Emerging markets in Asia and Africa provide strong growth prospects as governments prioritize railway development to meet urbanization demands.

Restraints:

- Lower density sleeper spacing in modern design reduces overall consumption.

- Environmental and regulatory concerns limit the adoption of certain materials in specific regions.

- High initial capital investment required for the adoption of advanced sleeper technologies poses challenges for smaller manufacturers.

Segmentation Analysis

The railway sleepers market is broadly segmented by product material type and end-use applications.

By Product Material Type:

- Concrete Sleepers: Holding the largest share, these are widely adopted for their strength, long lifespan, and cost efficiency, particularly in mainline rail projects.

- High-Strength Pre-Stressed Concrete Sleepers: Enhanced durability and higher load-bearing capacity make them ideal for heavy-haul rail networks.

- Steel Sleepers: Lightweight and suitable for flexible or specialized installations, though less common compared to concrete.

- Wood Sleepers: Traditional option still in use for landscaping and lighter tracks, though declining in railway applications due to environmental concerns.

- Composite and Plastic Sleepers: An emerging category gaining traction because of sustainability benefits, vibration absorption, and recyclability.

By End-Use Application:

- Railway Networks: The dominant segment, including freight, passenger, and high-speed rail systems.

- Landscape and Decoration: Utilized in gardens, parks, and private properties for functional and aesthetic purposes.

- Mining Applications: Heavy load resistance makes sleepers crucial for track infrastructure in mining industries.

- Urban Transit Systems: Specialized sleepers are used in metro, commuter rail, and LRT systems where vibration control and durability are critical.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/113617/

Country-Level Analysis: USA and Germany

United States:

The U.S. railway sleepers market is valued at over USD 14 billion, supported by expanding commuter rail and landscaping applications. Investment in infrastructure modernization, particularly for freight corridors and urban rail systems, continues to drive demand. Concrete remains the material of choice due to lifecycle advantages, though composite sleepers are gradually gaining ground as sustainability standards tighten.

Germany:

Germany is one of the most significant European markets, recording a projected CAGR of nearly 7%. The country’s extensive high-speed and regional rail networks require constant upgrades, spurring demand for advanced sleeper materials. Environmental policies encourage sustainable materials such as composites, while Germany’s focus on innovation has also supported development of photovoltaic-integrated sleeper systems.

Commuter Rail Segment Analysis

Definition & Role:

Commuter rail systems connect metropolitan areas with suburbs and play a vital role in addressing congestion and environmental concerns in urban centers.

Drivers of Demand:

- Rapid growth of metro and suburban rail systems in Asia, Europe, and North America.

- Increased investment in sustainable transportation options to reduce traffic congestion and emissions.

- Passenger expectations for safety and comfort require sleepers that minimize vibration and noise.

Material Preferences:

- Concrete sleepers dominate commuter networks due to their robustness and low maintenance needs.

- Composite sleepers are being deployed in urban corridors for their vibration-absorbing qualities and compatibility with bridge and tunnel installations.

- Hybrid and innovative sleepers offer additional benefits such as energy generation and extended service life.

Regional Hotspots:

- Asia-Pacific: Large-scale metro and suburban rail projects drive significant commuter sleeper demand.

- Europe and North America: Urban renewal programs and commuter network modernization sustain steady market growth.

Press Release Conclusion

The Global Railway Sleepers Market is entering a dynamic growth phase, projected to nearly double in size from USD 62.5 billion in 2023 to USD 112.8 billion by 2030 at a CAGR of 8.8%.

This growth is anchored by the rise of metro and commuter rail systems, the expansion of light rail transit projects, and the continued modernization of freight and passenger rail infrastructure. Concrete sleepers remain dominant, while innovative solutions in composite, recycled, and photovoltaic-integrated sleepers are opening new opportunities for sustainable growth.

In regional terms, Asia-Pacific leads demand due to rapid urbanization and government investment, while Europe and North America continue to expand and modernize their rail infrastructure. The United States shows strong growth through freight and commuter rail, while Germany exemplifies Europe’s sustainable innovation drive.

With innovation, sustainability, and infrastructure investments at the core, the railway sleepers market is poised to play an integral role in shaping the future of global transportation systems. Industry stakeholders—including manufacturers, urban planners, and policymakers—are encouraged to leverage this momentum by aligning strategies with evolving market demands.