Semiconductor Etch Equipment Market Overview Analysis By Fortune Business Insights

Market Summary

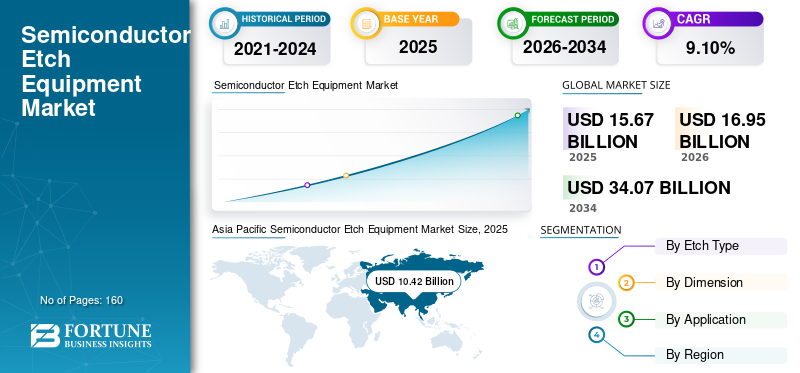

According to Fortune Business Insights: The global semiconductor etch equipment market was valued at USD 15.67 billion in 2025 and is projected to grow from USD 16.95 billion in 2026 to USD 34.07 billion by 2034, reflecting a compound annual growth rate (CAGR) of 9.10% over the forecast period. This robust growth trajectory is underpinned by escalating demand for advanced semiconductor chips, rising investments in domestic manufacturing, and the accelerating shift toward miniaturized, high-performance electronic devices.

Semiconductor etch equipment plays a central role in chip production, accounting for 50–60% of total wafer processing operations. These machines level wafer surfaces through two primary methods — dry etching and wet etching — and are widely used across semiconductor fabrication plants, electronics manufacturing facilities, and test homes.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/109530

Key Market Drivers

Miniaturization and Rising Semiconductor Demand The push for increasingly compact wafers and chips is one of the most significant forces propelling market growth. Industries such as electric vehicles (EVs), consumer electronics, connected devices, and home appliances are demanding more sophisticated and smaller semiconductor components. This has directly elevated the need for precision etching equipment capable of supporting sub-nanometer manufacturing processes.

Technological Advancements and AI Integration Post-pandemic, semiconductor etch equipment has found expanded application in next-generation technologies, including Artificial Intelligence (AI) and Industry 4.0 systems. Manufacturers are channeling substantial R&D investments into developing advanced equipment that can produce more compact wafers at higher accuracy and efficiency. South Korea, for example, announced a USD 6.94 billion government investment in AI in 2024, with a major focus on bolstering its semiconductor manufacturing capabilities.

Government Policies and Mega Investments Governments and major corporations worldwide are committing large capital to expand semiconductor manufacturing capacity. Intel Corporation announced plans to invest approximately USD 100 billion in new fabrication plants across U.S. states including Ohio, Arizona, New Mexico, and Oregon. The U.S. CHIPS and Science Act further incentivizes domestic semiconductor production, aiming to increase the country's global manufacturing share.

Market Restraints

Despite strong growth prospects, the market faces a notable challenge: heavy initial capital investment and delayed return on investment (ROI). Semiconductor etch equipment represents a substantial asset purchase that is beyond the financial reach of many small and medium-sized enterprises and start-ups, which can temper short-term demand growth.

Segmentation Analysis

By Etch Type The dry etch segment commands the highest market share. Dry etching offers superior process control, stronger isotropic precision, and uses gas instead of costly chemicals, making it both safer and more cost-effective than traditional wet methods. The wet etch segment, which held 56.70% of market share in 2026, remains relevant for conventional chip manufacturing and stable production lines.

By Dimension The 3D segment leads the market, projected to hold 41.95% of share in 2026, owing to its lower machining costs and ability to produce the thinnest, most compact chips for telecommunications and broadcasting applications. The 2.5D segment is expected to grow at a CAGR of 9.1% through the forecast period, while 2D technology is gradually being phased out as manufacturers transition to more advanced dimensional configurations.

By Application Semiconductor fabrication plants and foundries dominate, projected to capture 58.05% of the market in 2026. Their dominance is driven by surging global demand for semiconductors across consumer electronics, medical devices, and automotive sectors. The semiconductor electronics segment is anticipated to grow at a CAGR of 8.7%, supported by continued investment in chip manufacturing for a wide array of end-use devices.

Regional Insights

Asia Pacific leads the global market by a wide margin, accounting for 66.50% of revenue in 2025, valued at USD 10.42 billion. China, Japan, South Korea, India, and Taiwan are key contributors, with China alone representing USD 3.48 billion in 2025. The region benefits from concentrated R&D activity, dense manufacturing infrastructure, and aggressive government-backed investment.

North America is the second-largest market, reaching USD 2.82 billion in 2025 (18.00% share), and is projected to grow at a CAGR of 7.8% through 2034, supported by the CHIPS Act and a robust ecosystem of semiconductor firms and research institutions.

Europe contributed USD 1.67 billion in 2025 (10.70% share), driven by solid trade ties and growing government initiatives in semiconductor manufacturing. Germany is expected to be the region's largest contributor at USD 0.54 billion in 2026.

Middle East & Africa and South America are smaller but steadily growing markets, valued at USD 0.44 billion and USD 0.30 billion respectively in 2025, with increasing interest in establishing regional semiconductor manufacturing capacity.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/109530

Key Industry Players

Leading companies shaping the competitive landscape include Applied Materials Inc. (U.S.), Lam Research Corporation (U.S.), Tokyo Electron Limited (Japan), ASML (Netherlands), KLA Corporation (Netherlands), ASM International (U.S.), Hitachi High Technologies Corporation (Japan), Dainippon Screen Group (Japan), Ferrotec Holdings Corporation (Japan), and Canon Machinery Inc. (Japan).

Recent notable developments include Lam Research's 2024 launch of the world's first production-oriented Pulse Laser Deposition (PLD) tool, Applied Materials' 2023 collaboration with Ushio Inc. to expand semiconductor manufacturing capabilities, and Lam Research's Coronus DX platform for 3D NAND and advanced packaging launched in June 2023.

Outlook

The semiconductor etch equipment market is poised for sustained, accelerated growth through 2034. Driven by global digitalization, the AI revolution, geopolitical emphasis on semiconductor sovereignty, and the relentless miniaturization of electronics, demand for high-precision etching solutions will remain robust. The market's long-term trajectory reflects the semiconductor industry's foundational role in powering the technologies of tomorrow.