Smoothies Market Overview Analysis By Fortune Business Insights

Market at a Glance

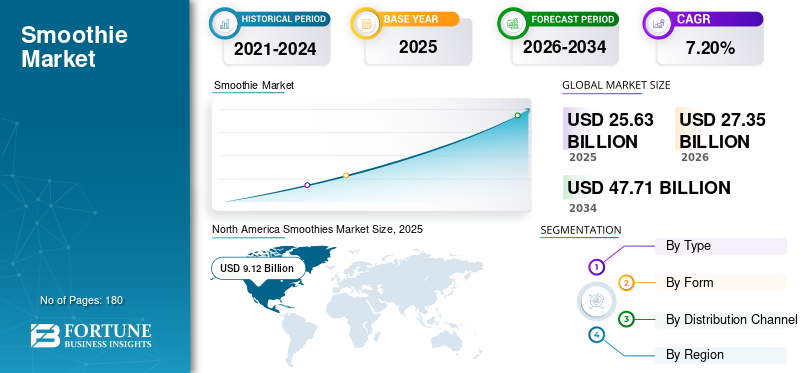

According to Fortune Business Insights: The global smoothie market was valued at USD 15.04 billion in 2025 and is forecast to grow from USD 16.47 billion in 2026 to USD 33.99 billion by 2034, reflecting a robust CAGR of 9.48% over the forecast period. This growth is underpinned by shifting consumer preferences toward convenient, nutrient-dense, and natural food options, with smoothies increasingly adopted as meal replacements, post-workout beverages, and everyday wellness drinks.

Key Market Drivers

Rising health consciousness is the primary engine of market expansion. Consumers are gravitating toward smoothies as accessible sources of vitamins, minerals, antioxidants, and plant-based proteins. Urbanization, busier lifestyles, and growing awareness of diet-related health risks have elevated demand for functional beverages. Smoothies now occupy a prominent space in clean-label and plant-based dietary patterns, appealing across age groups and income levels.

Commercial adoption has also deepened considerably. Cafes, smoothie bars, supermarkets, and quick-service restaurants have embedded smoothies into mainstream menus and retail shelves, strengthening the supply chain and broadening consumer access.

Get a Sample Research PDF: https://www.fortunebusinessinsights.com/enquiry/request-sample-pdf/111337

Market Segmentation Highlights

By Product Type, fruit-based smoothies dominate with a 45% share, driven by their natural taste, vitamin content, and versatility. Dairy-based variants follow at 25%, catering to protein-conscious consumers, while green smoothies — blending leafy vegetables and superfoods — account for 20%, buoyed by detox and gut-health trends.

By Distribution Channel, cafes and smoothie bars lead with 30% share, functioning as both primary consumption points and trend incubators. Supermarkets and hypermarkets hold 24%, supported by strong cold-chain infrastructure. E-commerce, though accounting for 14%, is the fastest-evolving channel, enabling subscriptions, frozen smoothie kits, and direct-to-consumer personalization.

By End User, lifestyle users and busy professionals represent the largest group at 34%, relying on smoothies for convenient daily nutrition. Fitness enthusiasts follow at 26%, with athletes comprising 18% of demand — both segments driving the functional and performance-oriented product segment.

By Age Group, consumers aged 15 to 30 account for the largest share at 34%, influenced by fitness culture, social media, and a taste for premium, experimental flavors. The 30–45 age bracket (27%) prioritizes balanced nutrition and convenience, while younger and older demographics add breadth to the overall market.

Regional Outlook

North America holds the largest share at 36%, reflecting a mature market with entrenched smoothie culture, strong retail penetration, and established brands like Smoothie King and Jamba Juice.

Asia-Pacific captures 28% and represents the most dynamic growth region, fueled by rapid urbanization, rising disposable income, and expansion of Western-style cafes. China leads within the region at 14% of Asia-Pacific share, while Japan commands 10%, with a preference for functional, portion-controlled formats.

Europe accounts for 26%, with Germany (9% of European share) and the United Kingdom (8%) as leading markets, where organic ingredients, clean labels, and sustainability heavily influence purchasing decisions.

Competitive Landscape

The market features a mix of global giants and specialist brands. Smoothie King leads with a 13% market share, followed by Danone SA at 10%. Other major players include The Coca-Cola Company, PepsiCo, Bolthouse Farms, Jamba Juice, The Hain Celestial Group, and Barfresh Food Group. Competition centers on ingredient transparency, functional innovation, sustainable packaging, and channel diversification.

Key Trends Shaping the Market

- Functional enrichment: Probiotics, adaptogens, plant proteins, and immunity-boosting ingredients are increasingly standard in new product launches.

- Plant-based expansion: Dairy-free smoothies using oat, almond, and coconut bases are gaining rapid traction.

- Ready-to-drink and frozen formats: Convenience-driven consumers are embracing packaged and frozen smoothie kits.

- Personalization via e-commerce: Subscription models and digitally tailored nutrition offerings are reshaping distribution.

- Sustainability: Eco-friendly packaging and responsible sourcing are becoming decisive brand differentiators.

Challenges and Restraints

High ingredient costs — particularly for superfoods, fresh fruits, and plant-based proteins — remain a barrier to wider adoption, especially in price-sensitive markets. Cold-chain requirements and short shelf lives increase operational complexity. Regulatory compliance around health claims, nutritional labeling, and allergen disclosures also adds layers of operational burden for manufacturers operating across multiple geographies.

Connect with Our Expert for any Queries: https://www.fortunebusinessinsights.com/enquiry/speak-to-analyst/111337

Investment and Growth Outlook

The smoothie market presents compelling investment opportunities across production, cold-chain logistics, digital commerce, and functional formulation. Emerging markets offer untapped potential for affordable, regionally adapted products. The convergence of wellness culture, e-commerce growth, and functional nutrition trends positions the global smoothie industry for sustained, broad-based expansion through 2034.